BioSante Pharma BPAX Stock ResearchIntroduction and Financials

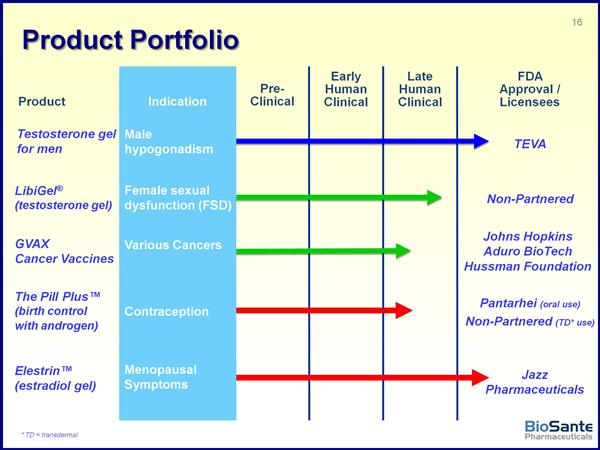

Cancer Vaccine (GVAX) portfolio Other Products and Pipeline assets Libigel - Background and Business Development Libigel - Clinical Trials BioSante Pharma (BPAX)Website link: www.biosantepharma.com

Archive of all BPAX related blog posts and articles: Blue font denotes premium content for Chimera Reserch Group subscribers. Citi Healthcare webcast 3/5/11 - click here for my notes 4q2010 earnings 3/16/11 - click for PR link (no cc) JMP webcast 5/9/11 - click here for my notes 1q2011 earnings 5/10/11 - click here for PR (no cc) UBS webcast 5/24/11 - click here for my notes Stifel Nicolaus webcast 9/7/11 - click here for my notes. Rodman and Renshaw 9/12/11 - click here for my notes. JMP Securities webcast 9/27/11 - click here for my notes. Immunotherapy webcast 10/6/11 - click here for my notes. BioCentury webcast 10/21/11 - click here for my notes. BIO Investor webcast 10/26/11 - click here for my notes. BIO CEO conference 2/2012 - click here for my notes. Roth Capital Growth conference 4/2012 - click for my notes. 5/2012 ASCO preview and review of 1q2012 results - click for blog. 5/2012 ASCO abstract - click for blog. |

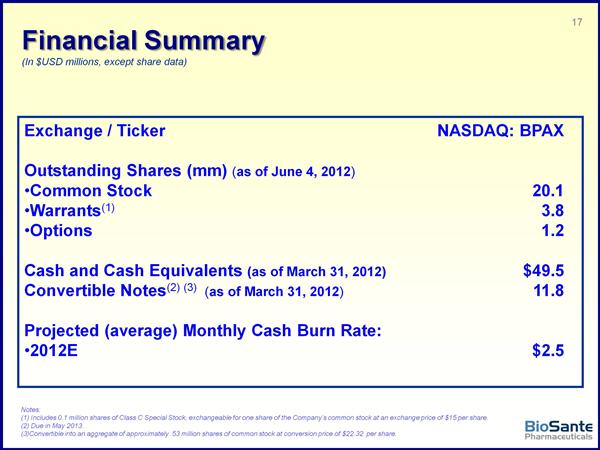

ValuationShares Outstanding: 116.3 million (as of 2/8/2012)

Fully Diluted Share Count: 138.72 million (23.2m warrants and 7.3m options as of Feb 2012) Recent quote: $0.68 Market Cap: $79.1 million Estimated Cash: $57.2 million (as of 12/31/2011) Total Debt: $15.8 million (as of 2/8/2012 and due 5/1/2013, convertible at $3.72/share) Estimated Net Cash: $41m Estimated Enterprise Value: $38 million (4/6/2012) 2012 cash burn is $2.5m per month as long as the LibiGel safety study continues |

June 2012

June 2012

June 2012

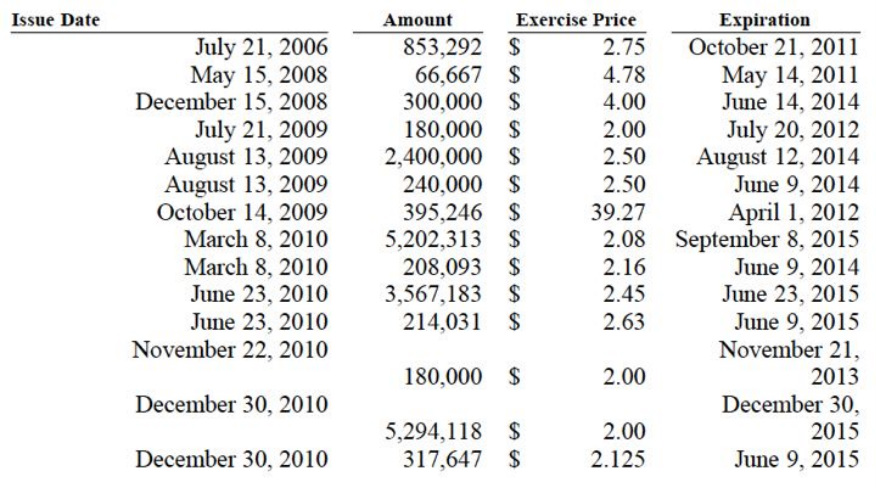

BPAX has a frequent history of dilution

These values are not adjusted for the 2012 reverse stock split!

- A $75m shelf was filed 5/24/2010, of which ~$58m has been used as of May 2011. Filed new $150m shelf 5/27/2011, usually becomes effective ~20 days (click for info) and expires after 3 years (hat tip to @BioTrader9)

- August 2009 sold 6m shares and 2.4m warrants at $2.00 for net proceeds of $11.1m

- March 2010 sold 10.4m shares and 5.2m warrants at $1.73 for net proceeds of $17.5m

- June 2010 sold 7.1m shares and 3.55m warrants at $2.10 for net proceeds of $14.2m

- December 2010 sold 10.6m shares and 5.3m warrants at $1.70 for net proceeds of $16.9m

- March 2011 sold 12.2m shares and 4.0m warrants at $2.0613 for net proceeds of $23.8m

- Have $25m or 5.4m share equity standby agreement with Kingsbridge that expires in December 2011, issue at 8-14% discount. Had not sold any shares as of 12/31/10.

- 3/15/11 webcast: fully diluted share count is ~123 million

- Take into account also the $22m in convertible debt shown above (and detailed in the 2nd table below) and the numerous warrants summarized in the table below (note the table does not include the March 2011 warrants):

June 2012

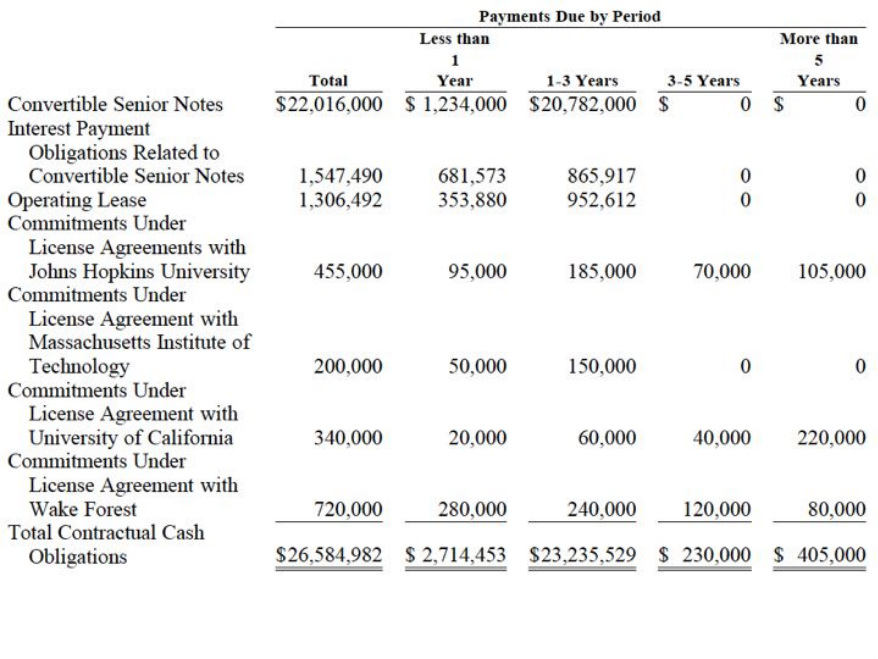

Source: 2010 10k

Management

|

General and Outlook

- 2010 10K: "We expect to continue to incur substantial and continuing losses over the next 18 to 24 months as our own product development programs continue and various preclinical and clinical trials commence or continue, including in particular our Phase III clinical study program for LibiGel"...."We currently do not have sufficient cash resources to obtain regulatory approval of LibiGel or any of our other products in development....we believe that our cash and cash equivalents of $38.2 million at December 31, 2010 and the additional $23.8 million in net proceeds we received from our March 2011 registered direct offering will be sufficient to meet our liquidity requirements through at least the next 15 to 18 months"

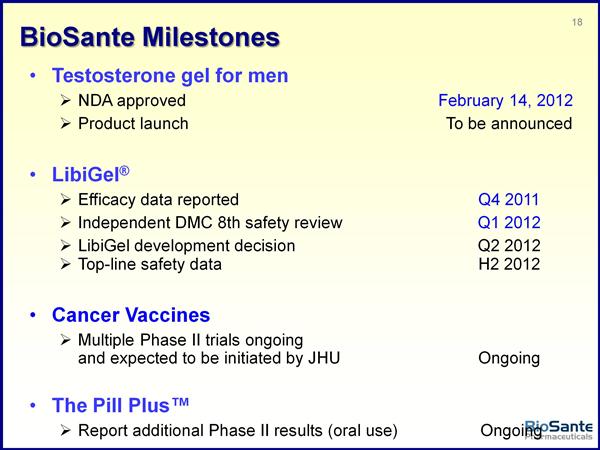

- R&D expenses of $3.5-4.5m per month until safety study is enrolled, falling ~30% to about $3m late 2011 and into 2012 (4/15/11 and 5/24/11 webcasts)...only see safety study patients yearly after 12 months, greatly reduces costs

- 3/15/11 and 4/15/11 webcast: Cash on hand is sufficient to get to 3q2012. 5/24/11 webcast: "No intention or need to raise money in 2011"

- Merger w/ Cell Genesys $CEGE announced 6/30/2009 and closed 10/15/2009- issued 20.2m shares valued at $39m

- 9/14/2010: 40 employees (35 on libigel). 12/31/10 45 employees, 38 involved in product development

- Previously have said that will probably partner Libigel before NDA (catalyst would be completion of enrollment), definitely before aproval, or complete sale of company

- 2010 10k: "Marketing rights to our gel products in Canada are subject to an agreement with Paladin Labs Inc. [September 2000] In exchange for the sublicense, Paladin agreed to make an initial investment in our company, make future milestone payments and pay royalties on sales of the products in Canada. The milestone payments are required to be in the form of a series of equity investments by Paladin in our common stock at a 10 percent premium to the market price of our stock at the time the equity investment is made." [I have never heard any discussion of this arrangement before]

- R&D expenses were $39.7m in 2010, $13.7m in 2009, and $15.8m in 2008