Navigate the Ligand Pharmaceuticals, Inc. ($LGND) Stock Research Pages

- Introduction (valuation, financials, ownership, guidance, helpful links)

- Promacta (eltrombopag) (key asset licensed to GSK - platelet booster for many thrombocytopenia conditions)

- Kyprolis (carfilzomib) (key asset licensed to Amgen - developed by ONXX for multiple myeloma)

- Other Marketed Products (description of assets currently generating royalty revenue)

- Late-stage Pipeline Assets (generally partnered and developed at little to no cost to LGND and represent future royalty sources)

- Early-stage Development Programs (internal and partnered, future "shots on goal" or out-licensing opportunities)

- Acquisitions (Cydex, Metabasis ($MBRX), Pharmacopeia ($PCOP), Neurogen ($NRGN) - complete terms and details)

- Captisol-Cydex (additional info on the formulation technology acquired in 2011 and details on partnerships)

- Discontinued Programs (with >90 biotech and pharma assets in development, not everything works out!)

Ligand $LGND history of mergers and acquisitions

Ligand as we know it today has been assembled via acquisitions of companies with numerous assets and then developing and out-licensing these programs as appropriate. The terms of the various mergers can be found below. Note that several of the deals involved Contingent Value Rights (CVRs) that entitle legacy shareholders of these companies to receive additional cash in the event of certain future achievements. Details about the clinical and commercial programs and other assets acquired in these deals can be found by following the links at the bottom of this page.

Cydex: January 2011 transaction details

- Privately held. Technology originated at Univ of Kansas but 8/2004 amendment ended royalty payment obligations of Cydex.

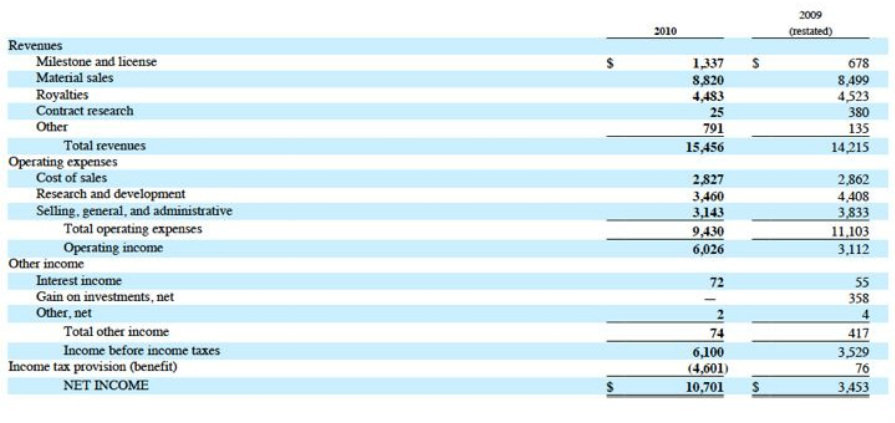

- 2010 revenue of $16.3m (made up of royalties, material sales, license fees, milestones) and EBITDA of $7.6m.

- As of 12/31/10 Cydex held $14.3m cash and $2.9m net accounts receivable. But the cash balance of $17.7m at closing was distributed to the Cydex shareholders account (ie, same as CVRs). Click here for 8k filing that includes Cydex accounting and balance sheet info. Click here for a 2nd, related 8k. Notes appear to say that in 2010 Cydex had $10.7m of product returned! Will have to dig into this more.

- In 2011 this deal will more than double LGND revenue.

- $32m cash paid upfront, additional $4.3m due 1/25/2012, plus contingencies (CVRs).

- Funding via $20m loan from Oxford (8.64% fixed- pay interest only starting immediately, starts amortizing on 3/1/12 unless opt to start 3/1/13 [notify by 1/24/12], matures 8/1/14- so 18 or 30 month term, 2% prepay fee 1st yr, 1% thereafter, no partial prepayment allowed, plus $1.2m final payment, secured by everything but IP).

- Borrowed additional $5m from Square 1 Bank in March 2011 at prime plus 200bp, interest paid monthly and matures 3/29/2012. 4/2011 increased this loan to a total of $10m- rest of terms unchanged.

- Will operate as subsidary w/ 9 employees.

- Contingent Value Rights (CVRs):

2) 20% of Cydex rev's between $15-35m until 2016 (30% after $35m)-but excludes other CVR payments

3) Clopidigrel licensing by 12/31/2016 (50% of upfront unless a certain potential partner=The Medicines Co by 4/25/11, then 100% up to $1.75m; 50% of milestones)

4) Cydex revenue sharing: From 2011-2016, 20% of revenue >$15m plus additional 10% of revenue about $35m [excludes other CVR payments]

- Deal requires 5 FTE and $1.5m annual investment thru 2015 unless <$10m rev 2011 or 2012 or <$15m rev 2013 or 2014.

- 3/31/11 10q: current estimated present value of CVRs is $19.2m

source: 2008 cydex IPO prospectus

source: 4/2011 LGND 8k

Cydex: Background info

- 2008 article and S1 prior to IPO:

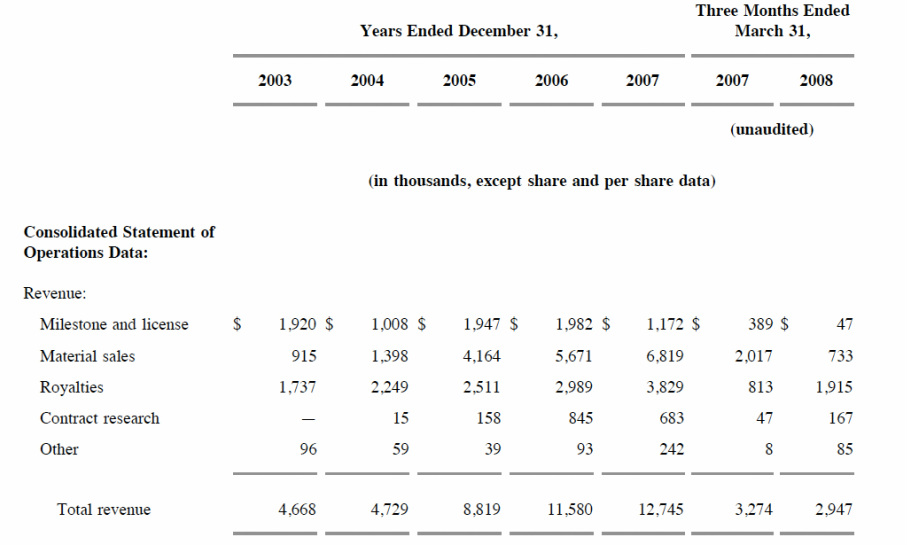

- 30 licensing deals, 2007 rev of $12.7m (S1: royalties of $3.8m in 2007, 3.0 in 2006, 2.5 in 2005, material sales of $6.8, $5.7, $4.2m)

- focus internal pgms only on acute care hospital market, and pair captisol w/ off-patent drugs

- 12 internal products at that time, 6 that plan to keep (inc cerebyx aka fosphenytoin for seizures- allow RT vs 4C formulation), and 6 intend to license. Company was profitable in 2006.

- PFE and other deals- royalties decrease or eliminated after patent expiration.

- PFE accounted for 27% of rev in 2006 and 40% in 2007; BMY 9% 2006 and 4% 2007.

- Competing technologies include hydroxypropyl beta cyclodextrin marketed by Janssen Pharmaceuticals, natural cyclodextrins, liposome technologies, emulsifier technologies and nanoparticle technologies.

- Rev recog policy: 2012 is earliest anticipated generic competitor.

- 1q2007 $347k milestones represented Abilify EU registration and two upfronts from one collaborator.

- 1q2008 $48k represents one upfront and one option fee.

- 2007 had $710k of back royalties from PFE

- 2010 10k: Cydex supporting drug development efforts with >40 companies worldwide

Metabasis $MBRX (January 2010)

- Acquired 1/2010 for $1.6m cash and additional contigency payments

- CVRs: 1) 65% of milestones/royalties from Roche; 2) 50% of proceeds from TRbteta; 3) 30% of MB07133 proceeds; 4) 60% of Pericor disposition; 5) 25-50% of proceeds from other pgms).

- 3/31/11 10q: estimated present value of CVR liability is $1.7m

- A few other early programs not discussed separately (MB07803 for diabetes; DGAT1 inhibitors for obesity).

- Must spend $8m on pgms between 1/2010 and 7/2013 ($3.9m so far as of 3/31/11).

- 2010 10k: HepC nucleoside analog in p1 "other internal pgm awaiting devel by LGND or partner"- which MBRX drug is this?

- Received $6.5m milestone from Roche 4/2010, 65% paid to MBRX CVR holders

- Deal includes Chinese licenses for pradefovir and MB07133, nonexclusive HepDirect license for HBV/HCV/HCC for China and ROW, right of 1st negotiation for other LGND assets in China

- $1m upfront (1/2 by 4/6/11, 1/2 by 12/31/11, and $25k/yr every Jan). 25-50% flows thru to MBRX CVR holders starting 7/1/2011 ($331k of upfront-50% of pradefovir, 30% MB07133, 40% general/license).

- Received $0.5m from Chiva 3/2011 ($150k for Pradefovir and $350k for MB07133), $0.1m paid to MBRX CVR holders

- LGND receives 5% of sub-licensing income for ex-China deals [includes all income- fees, milestones, royalties, equity, etc]

- LGND receives 8% royalties for Pradefovir and 5% royalties for all other products. Subject to reduction if generic drug enters market.

- Chiva gets right of first negotiation for additional applications of HepDirect technology and for the license of other LGND candidates for the Chinese market...At such time as LGND offers Chiva this offer of a "China Business Opportunity" for a LGND product, Chiva will issue LGND 10% equity in the company

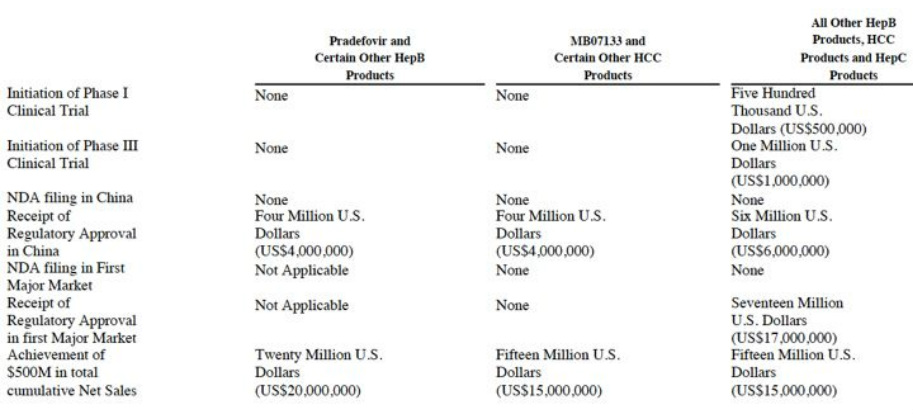

- Up to $100m milestones are possible [see table below]. Milestones can only be paid once for each product, but are due for each individual product, even if there are >1 products in a given column category

- 9/2011: deal amended: Requires $0.5m payment by 9/1/2011 vs 12/31/2011 (0.1m paid to MBRX CVR holders). Increases royalties to 6% and 9% (Pradeefovir). Eliminates provision that could have resulted in 10% stake for LGND.

source: license agreement appended to 1q2011 10q

Neurogen $NRGN (December 2009)

- Acquired 12/09 for 4.2m shares (equals 0.7m post reverse split), $0.6m cash, and contingency payments

- CVRs related to sale of real estate; sale of aplindore pgm; $3m for VR1 p3 or 50% proceeds of sold earlier; $4m on H3 partnering or 50% of proceeds.

- 3/31/11 10q: estimated present value of CVR liability in $0.7m

- Rec'd $7.4m cash and $180m NOL.

- 2/2010 sold their headqtrs for $3.5m cash and distributed as one of the CVRs.

- AIDD technology is old and has been supplanted, req's ppl and infrastrcture expense, so little real interest

Pharmacopeia $PCOP (December 2008)

- Acquired for 18m shares (equals 3 million post reverse-split), $9.3m cash plus additional contingency payments up to $15m (monetization of DARA by ye2011) - click here for PR.

- Former Organon partnership (now Merck) has concluded, but would get $ from advancement of programs with established lead.

- Ditto for Cephalon collaboration.

- 10/2010 combichem library and HTP screening tech sold for $1.8m ($0.8 deferred) plus 10% of collaboration revenues for 3 yrs (10/2010 comments: had discussions w/ 20-30 groups- bought by new startup who wanted equipment and hired the former LGND staff, this technology was also getting old, many companies have advanced compounds out of this library- so some sections of library carved out and excluded)

- GSK collaboration 3/2006: royalties 6% (<$500m) to 10% (>$3B), can be stepped up to 10-14%. Cannot screen compound library against the selected targets except for GSK. 8 compounds nominated ($0.5m milestone each, 2 in 2009). 9/2010: GSK terminated collaboartion (was to go to 3/2011), LGND keeps rights to develop the compounds

- What royalty rate can we expect Ligand to earn on deals they acquired via Pharmacopeia? Let's go to PCOP language from annual reports (this one for 2003, filed under Accelrys name before they spun out PCOP operations):