Navigate the Isis Pharma ISIS Research Pages

- Introduction (valuation, financials, outlook, company catalysts)

- Antisense background (science, technology, intellectual property, manufacturing)

- KYNAMRO - mipomersen (lead program in regulatory review for familial hypercholesterolemia)

- Mipomersen Liver Safety (special feature pages with extensive notes on long-term safety and efficacy of the drug)

- Cardiovascuar Disease pipeline (addtional CV drugs besides mipomersen)

- Metabolic Disease pipeline (several drugs for type II diabetes, as well as obesity)

- Cancer pipeline (including partnered with Eli Lilly $LLY and OncoGenex $OGXI)

- Severe, Rare, and Neurodegenerative Disease pipeline (incude GSK collaboration)

- Licensing deals and Satellite/spin-off companies (key business development activities)

- Discontinued Programs (not everything works out when you have a large and broad biotech portfolio)

Satellite Companies, Joint Ventures, and Out-licensed technology

- The four franchises above are the core focus of ISIS. However, ISIS utilizes its technology, IP, manufacturing, etc to form other partnerships that provide additional upside to shareholders at no or little cost.

- I have arranged these sections roughly in the order of highest to lowest potential value to ISIS shareholders.

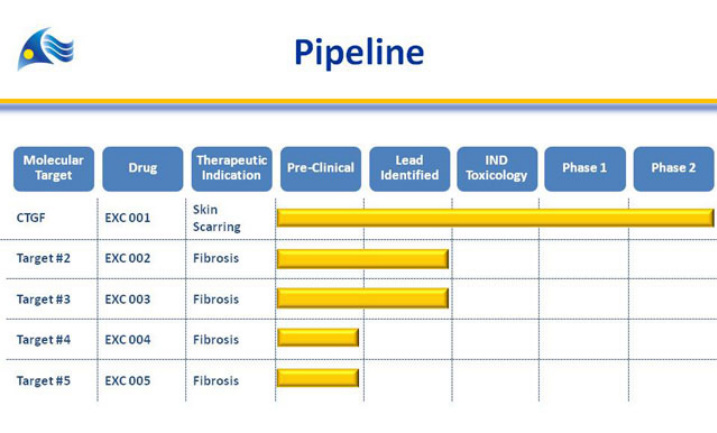

Excalliard (drug: EXC 001)

- Click here to visit Excalliard website

- private, ISIS owns ?? (<10% at 12/31/10). 11/2007- Collaboration and license for rights to various targets in treating local fibrotic diseases including scarring (see pipeline figure below), received equity as upfront payment plus $1m for target. Due up to $10.5m milestones plus royalties and sublicense income. 2010 10k: participated in financings in 2010 and 2011 to maintain same ownership stake.

- EXC 001 drug candidate against connective tissue growth factor (CTGF)- overexpressed in damaged skin/tissue. Developing for post surgical scarring and fibrotic disorders- administered into dermis

- IND 4/2009, p1 in healthy pts completed, three multicenter p2 POC trials started 4q2009

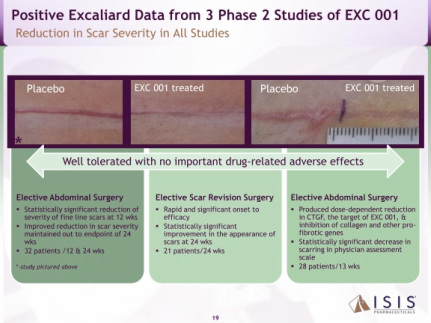

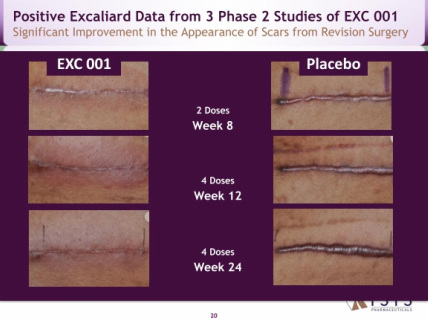

- 8/2010: positive interim data for study #202: 12 wks post abdominal surgery (doubleblind, 33 pts. visual analog by Pt/Dr/Indpt panel-stat sig less fine line scarring than placebo for all 3-even though not powered to be).

- 1/2011: released positive final p2 data for all three trials (click here for press release):

#202: 24 wks, maintain reduction in scars, but also true in placebo- so only speeds improvement.

#201: biomarker study- 28 abdom surgery pts.

- 11/2010: No comment yet on p3 pgm, maybe more dose optimiszation in p2, need end of p2 mtg w/ fda, begin p3 by 2012. 2010 ISIS 10K did not mention future plans.

- 5/2011: a new clinical trial appears online (click here for link). This randomized, double blind, placebo controlled (within-subject) trial will enroll women undergoing elevtice revision for scars from previous breast surgeries. Plans for 56 pts, estimated completion May 2012. There has been no PR from the company about this trial yet

- 6/2011 Annual meeting poster: projected NDA filing in 2015 (ouch, first time I had seen a date estimated for this...)

- Competitors:

- Shire/Renovo Juvista p3 data 1h2011- those companies are waiting for this before beginning 2nd p3 (and mixed p2 data).

- RXII Lead sdRNA program is based on same target and indication and is in preclinical development

5/10/11 BofA Merrill Lynch webcast - same images presented at 6/9/11 Jefferies webcast |

5/10/11 BofA Merrill Lynch webcast - same images also displayed at 6/9/11 Jefferies webcast |

Achaogen (drug: ACHN-490)

- Click here to visit the Achaogen website

- private, ISIS owns ?? (<10%). Developing antibiotics for drug-resistant pathogens.

- Raised 56m Series C 4/2010 (A/B rounds totaled $42m).

- 1/2006 Licensed "a suite of patents drawn to a class of chemically modi ed aminoglycoside small molecule antibiotics that resulted from the e orts of Isis’ earlier work identifying small molecules that target structured RNAs" for upfront fee of $1.5m Series A preferred stock

- Plazomicin aka ACHN-490 (next generation aminoglycoside aka neoglycoside for systemic, multidrug resistant gram negative bacterial infections). Broad spectrum activity, including against E. coli and methicillin-resistant Staphylococcus aureus (MRSA) - click to read article about the drugs progress. Click here for 9/2011 abstract presented at ICAAC.

- 1/2009 rec'd $1m milestone (half stock, half cash) for IND, potential for $33.5m more milestones, undisclosed royalties

- Successfully completed p1 and initiated 225 pt p2 initiated 3/2010 in UTI and pyelonephritis comparing against levofloxacin (triggered $2m milestone to ISIS).

- 8/2010: BARDA award $27m for 2 years, up to $64.5m total for development for plague and tuleremia

RNAi Collaborations with Alnylam $ALNY

- Goal: "Combine Isis’ & Alnylam’s intellectual property positions to enable Alnylam to develop dsRNAi therapeutics"

- 3/2004 licensed double-stranded RNAi (dsRNAi) technology to ALNY for $5m upfront fee plus milestones (up to $3.4m per drug), royalties, and share of sublicense income. Isis retains rights to certain dsRNAi targets. Click here for additional info on ALNY research page.

- ISIS made a $10m equity investment in ALNY at the time (all had been sold by 12/31/2010)

- 12/2010 received $0.375m milestone for p1 initiation of ALN-TTR drug

- 4/2009: single-stranded RNAi (ssRNAi) therapies collaboration. Rec'd $11m upfront plus $2.6m of research funding in 2009-2010. This portion terminated by ALNY in 11/2010 (avoided $10m milestone payments due starting shortly thereafter; dsRNA deal remains in place)

- 9/2011 presented ssRNA data at OTS meeting (click for details)

- "We continue to advance the development of ssRNAi technology and during the course of the collaboration, we made improvements in the activity of ssRNAi compounds, including increased efficacy and potency as well as enhanced distribution" (2010 10k)

- ALNY also provided license to Isis for their IP. Isis would owe up to $3.4m milestones plus royalties to ALNY if this is utilized. 2010 10k: no RNAi candidates in development

- As of 12/31/10 ISIS had received a total of $37.1m from ALNY ($26.5m in 2007 for ALNY deal with Roche - nearly 10% of upfront fee)

- 6/2011 Annual meeting: have received total of $54m in upfront fees, sublicensing revenue, and R&D funding to date

Santaris Pharma (formed by merger of Cureon and Pantheco in 2003)

- Click here to visit the Santaris website

- Click here to download 2010 Annual Report

- private, 12/31/2010 E17m cash and 89.9m shares ISIS owns ?? (<5%). No capital raise since Series C in 2007, was profitable in 2010.

- "In September 2000, we entered into an agreement to license our novel antisense chemistry, Peptide Nucleic Acid, or PNA, to Pantheco, on a nonexclusive basis to treat diabetes and cardiovascular diseases [limited # of targets subject to approval by ISIS]. Pantheco completed financing to raise funds to support its current business and to fund this expansion of therapeutic focus on October 18, 2000. Subsequent to the

- completion of Pantheco's financing, we received, as a fee for this license, 9 million DKK, or $1.1 million, which was paid in Pantheco shares [40,000]. In addition, Pantheco will pay us royalties and milestones on any products developed using PNA. This is the second license of PNA technology from us to Pantheco. As part of the first licensing transaction completed in November 1998, we received an equity position [24.9%] in Pantheco." 2000 10k...This brought total equity stake to 22% at 12/31/2000. 12/31/2001: 18% ownership. 12/31/2002: 15.5% 12/31/2003 <10% after merger

- Locked Nucleic Acid platform main US LNA patent expires 2017. First company with drugs targeting both mRNA and microRNA in the clinic

- LNA is a modification of RNA that contains an oxymethylene bridge between the 2’ and 4’ carbons in the ribose ring. This bridge creates a bi-cyclic structure that locks the conformation of the ribose and is the key to the high stability and affinity of LNA to its complementary RNA sequence. The most important features of LNA antisense oligonucleotides commonly observed across molecules of this class include: excellent specificity to the drug target, increased affinity to drug targets providing improved potency, favorable pharmacokinetic and tissue-penetrating properties that do not require complex delivery vehicles, scalable and cost-effective manufacturing, well tolerated, potential for oral delivery (Santaris 2010 AR)

- 9/2011: ISIS sues Santaris for patent infringement (Press release - Complaint court document)

- Partnerships cover 25 targets, 10 of which Santaris has delivered drug candidates for so far

- Unpartnered drugs for metabolic indications: Started p1 trials in 2011 for candidates targeting ApoBIII (SPC4955- click here for PR) and PCSK9 (SPC5001 - click here for PR)

- Wyeth (now PFE) partnership 1/2009 for up to 10 undisclosed RNA-targeted therapies (worldwide, $7m upfront, $10m equity, up to $83m possible milestones per target, double digit royalties). 1/2011: deal expanded ($14m additional upfront, $600m milestones for up to 10 new targets).

- Several pgms have advanced from 2009 $PFE deal w/ early milestones achieved

- Shire partnership 8/2009 for up to 5 targets for rare diseases (worldwide, $6.5m upfront, $72m possible milestones per target [plus $13.5m more for initial studies], res funding, undisclosed royalties)

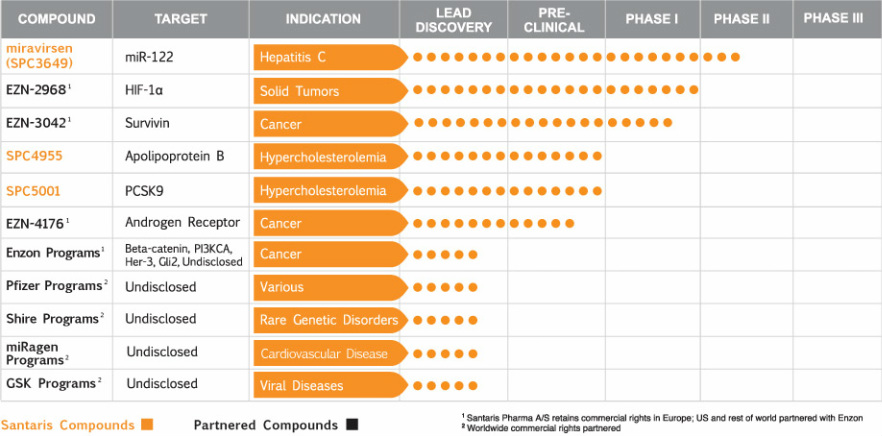

- Enzon alliance 2006 for 8 oncology targets (worldwide except EU, up to $200m upfront/milestones, high single digit royalties): delivered candidates for 6 targets in 24 months by 4/2009.

- ENZ2968 HIF1a p1 data 6/09. 2010 initiated p1 in collaboration with NCI

- EZN3042 Survivin p1 started 3/09 in solid tumors and lymphomas

- EZN4176 Androgen receptor. IND approved. Plan p1 in CRPC

- SPC2996 Bcl2 two p1/2 complete in CLL.

- GSK option deal in 2007 for up to 4 targets for viral diseases after p2a POC (worldwide, up to $700m upfront/milestones, high single to double digit royalties).

- SPC3649/miraversin: mir-122 for HepC- liver specific, required for viral replication (first micro RNA targeted drug in human trials), entered p1 3/2008- multidose ongoing at 4/2010, mechanistic POC achieved in humans, p2a started 9/2010 (RDBPC, multidose, US and Eur, 55 tx-naive pts weekly or biweekly for 4 wks). Linked to Regulus-GSK deal, if GSK options this compound, fees etc to Regulus/ISIS/ALNY. GSK declined this option and went with Regulus HCV candidate (click for details). November 2011 - phase 2a data presented at HCV (click for press release)

- 2010: miRNA partnership w/ Miragen for CV disease. Undisclosed equity stake, milestones, royalties

iCo Therapeutics (drug: iCo-007)

- Click here to visit the iCo website

- Click here for PDF of corporate slide deck (accessed 5/2011)

- public Canadian (TSX ICO.V), development stage company only, 41m shares outstanding 4/29/2011 (43m fully diluted). Had $2m cash ye2010 (click here for year end 2010 results PR). Announced $10m over 3 yrs equity line 4/2011 (iCo has discretion to issue new shares w/ a minimum price, no warrants). Cash burn is ~$0.6m per quarter

- 12/31/10 ISIS owns 12.3% after exercising warrants for 1.1m shares in 2010.

- iCo-007 antisense against cRaf kinase discovered by ISIS and licensed to iCo 8/2005 for eye disorders that occur as complications of diabetes. $0.5m upfront, up to $22m milestones, royalties.

- "In preclinical studies, antisense inhibition of c-Raf kinase was associated with a reduction in the formation and leakage of new blood vessels in the eye, suggesting inhibiting c-Raf kinase can improve treatment for both diabetic macular edema and diabetic retinopathy. Diabetic retinopathy is one of the leading causes of blindness in people in the U.S., and nearly 100 percent of type 1 diabetics by age 20 have evidence of retinopathy. Additionally up to 21 percent of people with type 2 diabetes have retinopathy when they are first diagnosed with diabetes, and most will eventually develop some degree of retinopathy." (2010 10k).

- Developing as intravitreal injection for diabetic macular edema (1.6m pts) and wet AMD. IND filed 12/2006 (triggered $0.2m milestone)

- P1 initiated 9/2007 (triggered $1.25m milestone paid as 0.94m shares of stock) and complete 5/2010 (4 US sites, 15 DME pts, single injection of 110/350/700 ug, no safety issues, efficacy signals-23% 5 letter improvement at 24 wks).

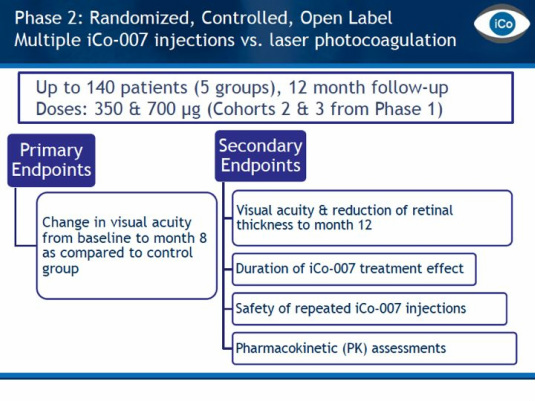

- 7/2010: recd ok from canada to conduct p2 trial (see figure below for summary of design), 4q2010 fill/finish commenced but will not start trial until raise funds. 2/2011 manuf complete for p2 trial. ISIS 2010 10k: iCo plans to initiate p2 in 2011..."Co slide deck says "early 2011"

- 8/2011: initiated IDEAL phase 2 trial at multiple US sites. Randomized trial of iCo-007 intravitreal injections alone or in combination with Ranibizumab or Laser Photocoagulation in the Treatment of Diabetic Macular Edema - click here for PR. 9/2011 announced undisclosed support for the trial from Juvenile Diabetes Research Fndn.

- Corporate slide deck references regional partnership discussions

- Also has -008 and -009 nonantisense pipeline candidates

Antisense Therapeutics Ltd (ASX: ATL)

- Click here to visit the ATL website - Click for notes from 2/2012 BIO CEO presentation.

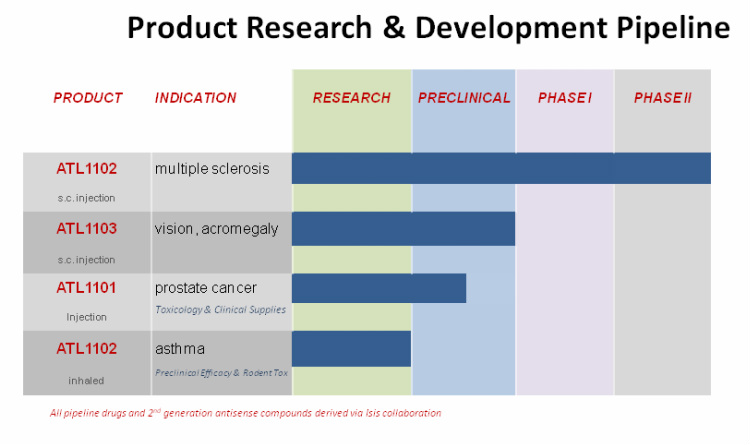

- public, ISIS owns 58.8m shares (<10%). Entire pipeline is generation 2.0 ISIS antisense molecules (see chart below).

- 10/2010: raised $2.4m in rights issue at $0.008 to fund ATL-1103, now 888m shares plus 120m new options. 3/31/11 has $2.5m cash on hand. 6/2011 raised A$0.5m (none to ISIS, 62.5m shares at A$0.008 plus 31.25m 18 month placement options at A$0.015 - Click for PR) to be used solely for ATL1103.

- ISIS received $0.8m milestones in fy2010 (not sure what this was for, not mentioned in 2010 10k)

- Note: there is also an Antisense Pharma in Germany, appears to have no relation to ISIS (http://www.antisense-pharma.com/index_e.htm)

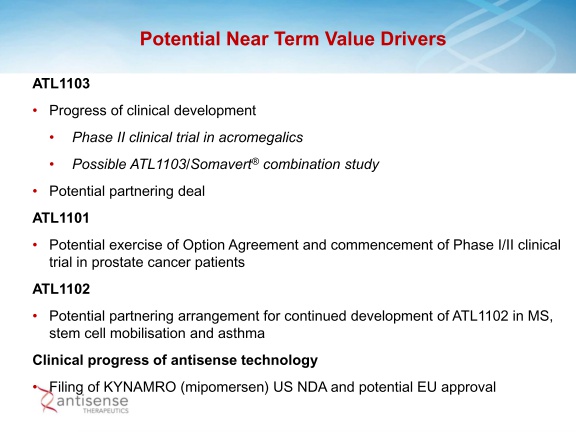

- ATL1101 (target is IGF-1R): preclinical- select tox studies are done and now trying to partner for prostate cancer.

- 9/2010: potential partner is evaluating drug in their animal models and hope they license. No mention in ISIS 2010 10k

- ATL1102 (fka ISIS 107248, target is CD49d subunit of VLA-4, licensed from ISIS 12/2001-eligible for royalties and sublicense income): intended for multiple sclerosis, same target as tysabri and running trials the same way:

- 6/2008: successful 8 wk p2a (reduced new active lesions)-

- 2/2008 partnered w/ Teva, but 3/2010 discontinued development. ISIS rec'd $1.4m sublicense fee 2008 and $2m for manufacturing in 2009.

- 9/2010 and 2010 10k: now seeking new partner for MS development. Also considering development of Inhaled formulation for asthma early stage (intend to outlicense, teva had and returned rights for this indication also).

- 9/2011: now applied for a patent for indication of "stem cell mobilization" to "enhance value to potential partners" (PR)

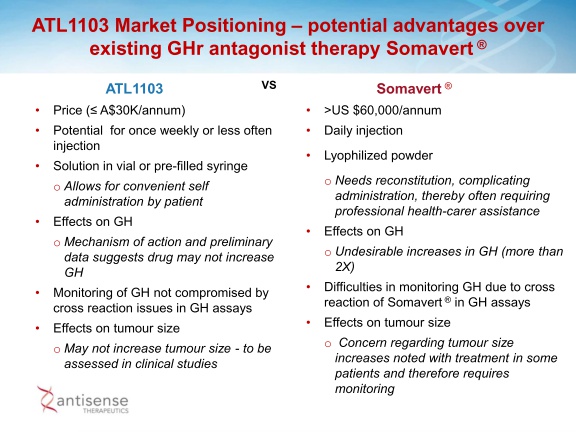

- ATL1103 (target is Growth hormone receptor -expressed in liver and reduces serum IGF1): preclinical, jointly discovered in collaboration w/ ISIS (eligible for royalties and sublicense income) for growth disorders (acromegaly- orphan drug, $30k/yr/pt=close to $1b) and vision disorders (diabetic retinopathy-multiB mkt).

- Animal tox done (started 5/2008) and drug supply for p1 has been manufactured (10/2009 ISIS rec'd $0.65m payment in form of 18.5m shares). 8/2010: this is pgm the company is spending on. 1220/10: with new funds work on formulation for injection and submit clinical trial application for 2011 start. 6/2011: Received approval for and started 36 patient phase 1 trial in Australia, will complete single and multiple ascending dose portions 1q2012 (Click for PR w/ trial details). 9/2011: single dose stage complete with 24 patients (placebo,25,75,250,400 mg - no SAE), multidose (6x250 mg doses in 12 pts, follow for 35 days) is underway, will report data by yearend 2011 (Click for PR)

- 12/2010 rec'd new US patent thru 2025

Fen 2012

|

Feb 2012

|

Archemix

- Click here to visit Archemix website

- Private, Isis does not have an equity ownership stake as of 12/31/10

- Focus on aptamer drugs "which take advantage of the three-dimensional structure of oligonucleotides to bind to proteins rather than targeting mRNA."

- 8/2007 Collaboration and strategic alliance w/ ISIS to utilize oligonucleotide technology and manufacturing for the development of aptamer drugs. Archemix received access to IP estate in exchange for equity, milestone payments, share of sublicense fees, and royalties

- Aptamer product candidates- several in p2 (11/2007 received $0.25m milestone for start of p2a and small milestone 5/2009)

- 12/2008 GSK deal $27.5m upfront ($6.5m equity), up to $200m milestones each of 7 targets including IL-23.

- Lead ARC1779 started phase 2b 1/2009 as anti-platelet for TMA rare disorder 100 patients.

- 11/2010: sold all hemophilia-related assets to Baxter, including ARC19499 (targeted against Tissue Factor Pathway Inhibitor) which began phase 1 trial 8/2010 in UK. $30m upfront payment, plus up to $285m milestones - click here for PR.

- 5/2011: journal article in Blood about ARC19499 as a procoagulant therapy - click here for details.

- 7/2011: BAX presented preclinical data on BAX499 (aka 19499). Expect phase 1 data 2h2011. Click here for PR.

Xenon Pharma

- Private - Click here to visit Xenon website

- 11/2010: new collaboration for anemia of inflammation targeting hemojuvelin and hepcidin (both targets expressed in liver and have been inaccessible via traditional; drug discovery). Undisclosed upfront convertible promissory note, eligible for sublicense/option fees, milestones, royalties

- "Anemia of Inflammation (AI) is a commonly acquired disorder that is associated with a variety of conditions including kidney disease, malignancy and other clinical settings of chronic inflammation. Currently available EPO-based therapies have dose-limiting side effects...To define novel therapeutic targets for the treatment of AI we studied the inherited disorder Juvenile Hemochromatosis (JH) as AI and JH represent opposite ends of the iron phenotypic spectrum. AI is characterized by iron-rich macrophages and impaired intestinal iron absorption which results in restricted iron availability for normal red blood cell production and anemia, whereas in JH, the macrophages are iron-depleted and intestinal iron absorption is enhanced, resulting in total body iron overload. Loss-of-function mutations in hemojuvelin and hepcidin were found to cause JH and as such, antagonists of either or both of these targets should reverse the iron disturbances in AI and treat the disorder in a new and more physiological manner." (Xenon website)

Atlantic Healthcare Limited (drug: Alicaforsen)

- Click here to visit website

- private, ISIS owns ?? (<20%, was 13.2% at time of licensing). Focus now seems to be on non ISIS-related pain drugs/abuse deterrents

- Alicaforsen (ICAM-1): First generation antisense targeting ICAM-1 (IV infusion)-overexpressed in UC/IBD and pouchitis. Previously failed two p3's by ISIS in Crohn's disease.

- 2007 licensed to Atlantic for pouchitis and potentially UC and other inflamm diseases ($2m upfront as equity, undisclosed milestones and royalties). Currently pursuing funding for pgm.

- FDA and EU orphan drug designation for pouchitis

- 10/2010: Clinigen named partner for named patient distribution of Alicaforsen in Europe for IBD

- Company is currently pursuing funding for future development

IP and Technology Sales, Out-licenses, and In-licenses

- Isis has an active intellectual property sales and licensing program. Customers have included:AMI, Idera Pharmaceuticals, Integrated DNA Technologies (IDT), Roche Molecular Systems, Silence Therapeutics (formerly Atugen AG), and Dharmacon (now a part of Thermo Fisher Scientific).

- 1/2009 sold former Ibis Biosciences diagnostics subsidiary to Abbott Molecular Inc $ABT (click here for Plex-ID website) for $215m plus earn-outs thru 2025 (5% of cumulative Plex-ID T5000 asset sales between $140m and $2.1b, 3% of sales over $2.1b, subject to reduction by up to 50% under certain circumstances). No revenue recognized in 2009 or 2010, so sales must still be below the $140m level.

- 1/2001 licensed patents (non antisense-related) to Eyetech necessary for the development of Macugen for opthalmic diseases in partnership with Pfizer $PFE. $2m upfront fee, $4m milestone in 2004 for NDA and FDA approval, up to $2.8m potential future milestones for other indications. Sold royalty rights for years prior to 2009 to Drug Royalty Trust 3 (received $24m between 2005 and 2007 plus share of royalties on sales >$500m [not sure this applied], get 100% of royalties starting in 2010), recognized $0.6m royalties in 2010.

- 10/2000 licensed certain chemistry patents to Roche Molecular Systems for use in diagnostic products for royalties ($1.8m in 2010).

- These transactions had generated >$398m as of 12/31/10

- Have in-licensed IP related to antisense and dsRNAi from and licensed RNaseH patents to Idera Pharma. Undisclosed financial terms

- 3/1999 in-licensed antisense patents from IDT, paid $4.9m licenses fees and would owe royalties until patent expiration 2/2013,